Part I: Introduction to the Swiss Real Estate Market

2. What Makes the Swiss Market Unique

2.1 Legal Stability and Low Volatility

Switzerland’s real estate market is widely regarded as one of the most stable in the world[1][2]. Housing prices generally experience slow, steady appreciation rather than sharp cycles. The country has avoided the kind of property bubbles and crashes seen in markets like the US, UK, or Spain.

This stability is supported by:

- A strong legal system and enforceable property rights

- Low population growth and controlled immigration

- Cautious fiscal policy and monetary oversight by the Swiss National Bank

- Limited land availability due to geography and tight zoning laws

Even during global shocks (e.g. the 2008 financial crisis or COVID-19), Swiss housing prices remained relatively resilient. Investors and homeowners alike benefit from predictable returns and minimal speculation, making property a conservative, low-risk asset class in Switzerland.

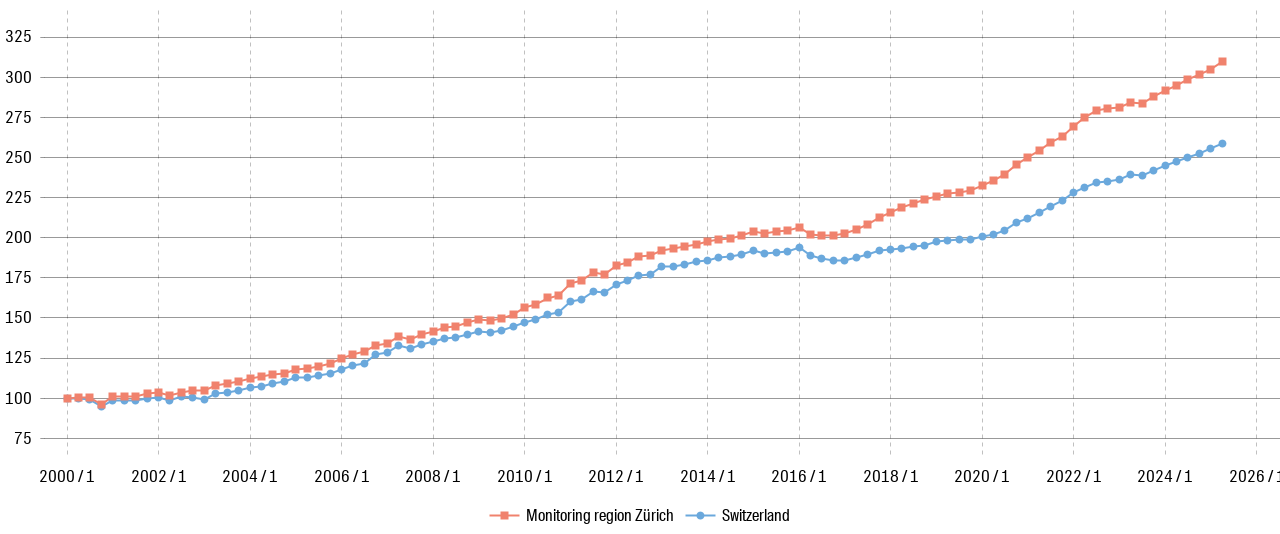

The FSO Residential Property Price Index (IMPI/IPIB)[3] for owner-occupied apartments illustrates this stability: prices show steady, low-volatility appreciation since 2017, even through global crises.

For a longer historical perspective, the Wüest Partner Hedonic Transaction Price Index[2:1] shows Swiss apartment prices since year 2000 — again demonstrating long-term stability with only gradual increases.

2.2 Strict Lending and Affordability Rules

Switzerland’s mortgage system is governed by strict affordability and risk-based rules, which help keep both borrowers and banks in check:

- Borrowers must provide at least 20% equity (of which 10% must come from personal, non-pension sources)[4].

- Total housing costs must not exceed one-third of gross income[5].

- Loans are typically interest-only in the first phase, with mandatory amortization down to 65% of property value within 15 years.

These rules are not just guidelines—they’re enforced by banks and audited by regulators. The result is a low rate of mortgage defaults, and a lending market that favors long-term sustainability over volume.

This also means that getting a mortgage can be challenging, particularly for foreigners or buyers with unstable income streams. However, once granted, Swiss mortgages are highly customizable, with a wide range of fixed, variable, and SARON-based products.

A full breakdown of mortgage options, tax considerations, and eligibility for residents and non-residents is provided in the Financing Your Apartment chapter.

2.3 Property as Long-Term Investment, Not Speculation

Unlike some international markets where property flipping is common, Switzerland strongly promotes long-term ownership. Key cultural and regulatory factors include:

- Capital gains taxes in many cantons discourage short-term resale (with rates decreasing the longer a property is held)[6][7].

- High transaction costs, such as notary fees and property transfer taxes, make frequent buying/selling unattractive.

- Limited tax advantages: While mortgage interest is tax-deductible, Swiss homeowners must also declare an imputed rental income known as Eigenmietwert — a theoretical amount they would earn if they rented their home to someone else. This significantly reduces the net tax benefit of ownership.

- Municipalities may impose minimum ownership periods or resale controls in designated areas.

Eigenmietwert is based on 60–70% of the market rental value and is included in taxable income at federal and cantonal levels. It has long been a subject of political debate and has faced multiple referendum proposals for repeal[8]. While still in force today, many expect reform or eventual abolition, particularly as homeownership among retirees grows.

As a result, Swiss buyers—whether private individuals or institutions—tend to hold properties for decades, using them for personal use, rental income, or inheritance planning. The market is not geared toward “get-rich-quick” investment strategies.

Even large institutional players (e.g. pension funds, insurance firms) view real estate as a stable yield asset, not a high-growth one.

2.4 Lex Koller and Foreign Ownership Restrictions

The Lex Koller law is a central piece of what makes the Swiss market unique—particularly for international buyers. It is a federal law that restricts real estate purchases by non-Swiss nationals unless certain conditions are met[9].

Key rules for individuals:

- Foreigners residing in Switzerland with a permanent residence permit (C permit) can buy property without restriction.

- Foreigners without residency may only buy:

- A single vacation home in designated tourist areas

- Property pre-approved by cantonal authorities

- Properties bought under Lex Koller are:

- Limited in size (typically under 200 m² of living area)

- Subject to resale restrictions, especially in the first 5 years

- No commercial or rental usage is allowed for foreign-owned second homes

Key rules for legal entities:

- Corporations, funds, and other legal entities are also subject to Lex Koller if they are:

- Foreign-controlled, or

- Headquartered abroad

- This includes Swiss-registered companies whose majority of capital or voting rights are held by non-Swiss persons. Such entities must seek prior authorization to acquire residential property, and are generally barred from buying property for non-commercial (i.e., housing) purposes.

- Swiss pension funds, foundations, and insurance companies—provided they are Swiss-controlled—are exempt and can freely acquire rental properties for long-term investment.

This means that foreign investors cannot bypass Lex Koller by simply setting up a Swiss shell company. Authorities will examine ultimate beneficial ownership and control, not just legal form.

Cantons such as Valais, Ticino, and Graubünden have zones where Lex Koller-approved projects exist. However, the total number of units available to foreigners is capped, and some municipalities (e.g. Geneva, Zurich) have fully banned foreign holiday home purchases.

Lex Koller is often confused with other restrictions, such as the Lex Weber (limiting the number of second homes in each municipality to 20%). Each canton applies Lex Koller differently, and some impose even stricter local rules or moratoria on foreign purchases.

Wüest Partner: Swiss Real Estate Report — quarterly market analysis: www.wuestpartner.com/insights/publications/real-estate-market-switzerland/ ↩︎

Wüest Partner: Hedonic Transaction Price Index — online query tool for apartments and single-family houses (2000–2025). https://www.wuest.io/online_services_classic/transaktionspreisindex/index_e.phtml ↩︎ ↩︎

FSO (BFS): Residential Property Price Index (IMPI/IPIB) — www.bfs.admin.ch/bfs/en/home/statistics/prices/property-price.html. ↩︎

SwissInfo: Mortgages in Switzerland: how the system works — www.swissinfo.ch/eng/demographics/mortgages-in-switzerland-how-the-system-works/89544500 ↩︎

UBS: The ABCs of financing: everything you need to know about financing your own home — www.ubs.com/ch/en/services/guide/mortgages-and-financing/articles/one-by-one-of-financing.html ↩︎

UBS: Real Estate Capital Gains Tax — ubs.com/ch/en/services/guide/mortgages-and-financing/articles/property-gains-tax.html. ↩︎

Comparis: Property gains tax in Switzerland: how is it calculated? — en.comparis.ch/immobilien/verkaufen/vertragsabschlussphase/grundstueckgewinnsteuer. ↩︎

ZKB: Abschaffung Eigenmietwert — Was würde der Systemwechsel für Besitzende von Renditeobjekten bedeuten? — www.zkb.ch/de/blog/immobilien/abschaffung-eigenmietwert-was-passiert.html. ↩︎

Federal Council: Lex Koller (SR 211.412.41) — www.fedlex.admin.ch/eli/cc/1983/823_823_823/en. ↩︎